This has been an exciting year for the e-mobility sector; gearing up for electrifying growth in the next few years. This article presents a snapshot of key happenings and trends in the global EV sales and manufacturing ecosystem, including battery cells, across various regions of the world.

Long before the advent of the COVID-19 pandemic, the global automotive industry has been undergoing tectonic shifts in certain critical technological and consumer preferences. This year has been turbulent for the industry on several counts due to the pandemic, but can also be considered more transformative for factors that are beyond COVID. Take, for instance, the 'surge' in EV sales happening since last year, in stark contrast to an overall decline in the global passenger vehicle market by 14 percent due to the pandemic.

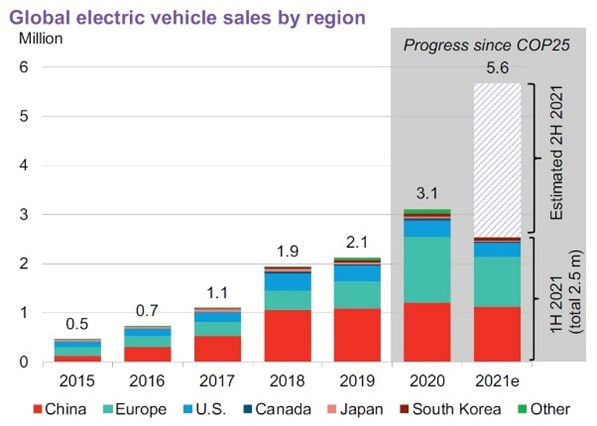

In the first half of 2021, over 2.5 million EVs were sold globally, about 140 percent more than that of H1 2019, and the estimates for the whole year stood at 5.6 million units (according to a special report by BloombergNEF). For sure, this EV surge is not necessarily pandemic-induced, but points to the emergence of a favorable macro-level environment – both in terms of technology and consumer demand – that can support the 'electrified' future of this industry.

But then, we have to acknowledge that the pandemic has forced automotive and venture capital companies to have a reality check on their market outlooks and emend their investments. High-value investments and partnership deals from leading OEMs and tech firms are pushing EV-related funding to new heights. As per CB Insights, funding to EV tech space has hit an all-time high of about $12.8 billion last year and is already approaching $9.8 billion at the beginning of the second half of 2021. A fair share of these investments is heading to the battery cell supply chain and R&D on new cell chemistries.

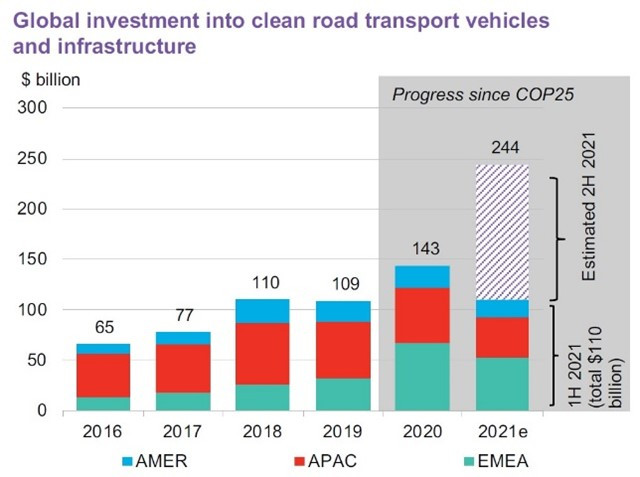

Further, US-based consulting firm AlixPartners expects a total investment of about $330 billion in the next five years throughout the EV supply chain, based on a five-year rolling average of all announced investments (as quoted by CNBC). On the other hand, cumulative investments in the global clean mobility ecosystem other than manufacturing and supply chain are expected to exceed $240 billion, more than double the investments in 2019. On the whole, there is likely to be a sudden rise in CAGR to around 22 percent in the forecasted 2021-30 period, with the e-mobility market surpassing $718 billion by 2030 (Precedence Research).

Leading geographies in these developments are Europe and China, which together are responsible for about 84 percent of global EV sales in the first half of 2021, followed by the US at 11 percent. China and Europe have led the global passenger EV and FCV market since 2015, and have stretched out their advantage in the last two years, visibly pulling ahead in terms of market share and absolute number of EVs sold. Japan, Asia-Pacific, and the rest of the world are comparatively lagging-behind in this regard.

On the investment front too, China and Europe are expected to top the figures this year, accounting for at least a third of investments heading to batteries and supply chain, followed by the USA. Thanks to the distressed global supply chain, automakers are investing significantly to localize battery cell production. In terms of EV ecosystem investments, the EMEA region is reported to have bagged much of it since last year - about $120 billion – followed by APAC and AMER regions witnessing $95 billion $38 billion respectively.

Asia Pacific

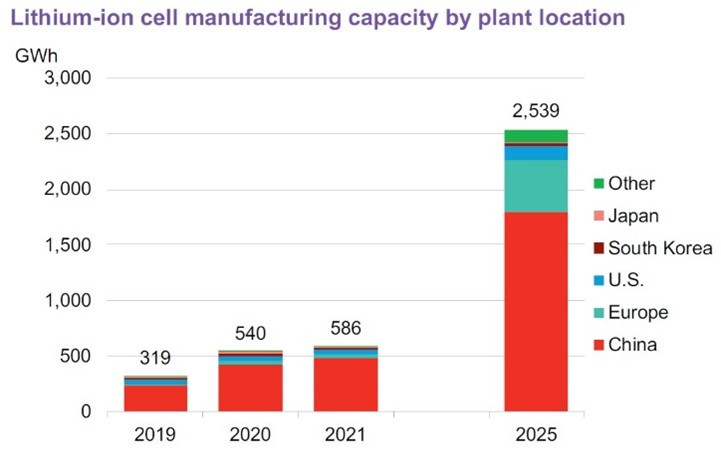

There is no surprise that China is the biggest market and manufacturer of electric vehicles, with an estimated parc of 5.5 million vehicles. The country is also the world leader in Lithium-ion battery production, with over 158 plants and 370 GWh capacity (2020) – about 77 percent of global capacity. It has been promoting domestic EV sales through New Energy Vehicle (NEV) credit and Corporate Average Fuel Consumption (CAFC) credit systems. Although, it is important to note that the country has been lowering its EV subsidies since 2019, including the 20 percent y-o-y reduction announced in the new EV subsidy policy for 2021. By 2022, there will be a subsidy cut of 30 percent.

That said, even without counting China, the APAC region is at the cusp of an EV revolution. Japan accounts for the second-largest share in the APAC EV market this year by value and volume, followed by South Korea. Australia, with a market size of 13,415 units this year (H1), has registered a y-o-y growth rate of 258 percent. Taiwan and New Zealand have recorded a growth rate of 33 and 163 percent respectively till August this year. Singapore has consistently strengthened its EV infrastructure including a robust charging network for public transportation. Southeast Asian countries like Indonesia, Vietnam, and Thailand are also emerging as strong players for EVs in the region, for e-2W.

For instance, Vietnam's electric bike start-up Dat Bike has raised $2.6 million early this year, while VinFast has sold around 50,000 electric motorbikes in 2020, prompting it to partner with LG Energy Solution for localized battery cell manufacturing. The country's annual e-2W production capacity already exceeds one million units.

Thailand is also aiming to seize the emerging EV manufacturing opportunity. It is attracting significant FDI with over 420 companies (2019) operating in the EV supply chain, while the country has 24 projects by various EV makers accounting to an annual capacity of 500,000 units, intending to grow EV manufacturing to 30 percent of total auto manufacturing by 2030.

From an investment point of view, since the valuations of large EV brands and their stock look stretched in recent years, investors find emerging companies and EV startups in the APAC region including India as attractive. In particular, companies that are involved in battery material processing and supply chain, along with those supplying common aggregates like lighting systems and other electronics for EVs, are seen as potentially attractive investments over the long term.

Russia

In August this year, the Russian government announced plans to develop its domestic EV market and target production of at least 28,000 units annually by 2024. Modeled on the lines of China's ZEV policy approach, the plan aims to offer subsidies to manufacturers of EVs, batteries, and hydrogen fuel-cell by covering the costs associated with special investment contracts and production facilities. Incentives are on offer for consumers as well, including toll-free roads for EVs from 2022 on a trial basis. The cost of the plan is estimated at RR590 billion ($7.9 billion), with private investments accounting for about RR500 billion ($6.7 billion). Further, efforts are in place to build at least 72,000 charging stations and 1,000 hydrogen filling stations in the country by 2030.

Europe

The European EV market overtook China as the world's largest in 2020 with a y-o-y growth of 137 percent to reach 1.4 million units, with a total parc of 4.1 million vehicles. Leading markets in Europe like Germany, France, and Italy have achieved significant growth of 22 percent, 16 percent, and 8 percent respectively in H1 2021, as against 2019 figures. The region is also known for its plug-in hybrid (PHEV) popularity, accounting for about 8 percent of passenger vehicle sales. One of the growth drivers for EVs in Europe is the stringent fuel economy targets revised in 2020 that require a 37.5 percent reduction in CO2 emissions by 2030. This is likely to be made even more stringent, which translates into a requirement of about 60 percent of new cars sales to be electric by 2030. The European Commission has also proposed to phase out the sales of ICE vehicles by 2035.

Further, Europe is rapidly emerging as a hub for cell manufacturing. It is estimated that the region's production capacity announced so far exceeds 1TWh by 2030, far exceeding the earlier forecasts. It is also reported that Europe may become self-sufficient with a realization of about 750 GWh and face the risk of overcapacity in the next few years, thereby risking new ventures and investments. However, manufacturers can bank on exports by countering the Asia production, currently dominated by China, South Korea, and Japan. European cell manufacturers also have to build up commensurate raw materials and cell components capacity alongside cell manufacturing, as the region is heavily reliant on imports from far-off regions including Africa, Chile, China, Australia, and so on.

The Middle East and Africa

Valued at $35 million in 2020, the EV market in Middle-East and Africa is expected to reach $ 84 million by 2026 with a CAGR of over 15 percent (Mordor Intelligence). Israel is the leading nation in this region, registering 10,083 units from January to August this year, with an annual growth rate of 154 percent. Turkey is yet another market exhibiting strong EV sales potentials. Both these countries, with considerable automotive and electronics manufacturing footprint, are eying investments in EV supply chain as well.

Saudi Arabia and Qatar are actively promoting foreign investments to establish a local EV manufacturing ecosystem. Saudi Arabia's $400 valued Public Investment Fund (PIF) has been active in the EV space for quite some time, including significant financing of over $1 billion to California-based Lucid Motors Inc. It was reported in January that PIF and Lucid are in talks to establish a factory near Jeddah. Qatar, on the other hand, aims to shift at least 25 percent of its public transport to electric by 2022, before the FIFA World Cup event, and 100 percent by 2030. It is in the process of establishing e-bus manufacturing to spur development. In August, Kuwait Ports Authority (KPA) has approved a proposal to build the region's first city to serve the needs of electric vehicle (EV) manufacturers.

Morocco, with its strategic positioning as a hub of the Europe-Africa automotive manufacturing value chain, is stepping up its EV-related investments. This year will mark the country supplying critical semiconductor chips to global EV makers including Tesla and Groupe Renault, manufactured by Franco-Italian semiconductor manufacturer STMicroelectronics. With carmakers like Dacia and Peugeot having immense production capacity in the country, Morocco is poised to become a leading player in the region's EV manufacturing scene.

The United States and Canada

North America is fast catching up with the EV wave emboldened by Asia and Europe. Supply chain disruptions in recent times are forcing US-based automakers to bring their supply chains to their local soil. Except for Tesla, other automakers were relying on Asian battery cell suppliers for their needs until now. With EV sales in the country picking up and the recent announcement by the Biden administration to invest $174 billion 'to win' the EV market, there is an added momentum in this regard. Some of the announcements in 2021 by companies in this regard are as follows:

- Ford Motor to invest about $11.4 billion in new U.S. ventures for EVs and batteries, including two lithium-ion battery facilities in central Kentucky through a JV with SK Innovation.

- Stellantis and LG Energy Solutions to form a JV to produce cells and modules in North America.

- Toyota Motor planning to invest about $3.4 billion in battery development in the US through 2030, including a new $1.3 billion battery plant.

- General Motors, partnering with LG Energy Solutions, is all set to begin cell production at its Ohio plan by next year. Another facility at Tennessee in the coming years.

- Taiwanese electronics giant Foxconn is purchasing an Ohio factory of EV startup Lordstown Motors for the production of EVs.

Canada, on the other hand, is fighting hard to make automakers invest in the country, as four of them have already finalized their investments in the US. The federal government has set an ambitious target to go 100 percent zero-emission in mobility by 2035. It is enticing automakers with a cleaner electricity grid and other manufacturing advantages. In Quebec, two lithium mines are under development, with UK-based Britishvolt planning to build a 60 GWh battery plant and Mississauga-based StromVolt eying to build a plant in the province. Lion Electric Company, which manufactures medium- and heavy-duty electric vehicles, hit headlines for a battery assembly plant in the country.

Given all staunch developments in the industry this year in terms of EV adoption and manufacturing across the globe, much of the success of the industry in the coming years is dependent on one critical factor – battery pricing. No doubt, the price of large-format lithium-ion batteries has fallen dramatically over the last decade. The volume-weighted average battery pack price in BloombergNEF's annual survey has decreased 89 percent since 2010, from $1,191 per kWh to $137 per kWh in 2020, which is a good sign. Based on an observed learning rate of 18 percent, prices of Li-ion battery packs could fall below $100/kWh in 2024 and reach $58/kWh in 2030. By 2035, lithium prices could drop to $45/kWh. But it's not that easy and simple as we might like to think. This requires material substitution and further technology advancements in cell chemistries. Localized battery manufacturing capacities, decentralized across key EV hotspot regions, need to grow steadily to meet the demand for stable, reliable, and low-cost procurement.