2020 the foundation-laying year for energy storage

It is time we look at the leading indicators rather than the lagging ones when it comes to implementing projects with energy storage. Else, we stand to lose out on yet another landmark opportunity to be a market leader.

The year 2020, will remain with all of us as a metaphor in life. As we have often heard people say: "Oh! It is 2020, anything but normal can happen." Of all the terrible things that happened throughout the year, one silver lining has been the growth of renewables and energy storage during this period. Renewables has been the only power-generating source which showed increase by 1 percent in generation share w.r.t 2019, while other sources like coal, oil, gas all saw decline.

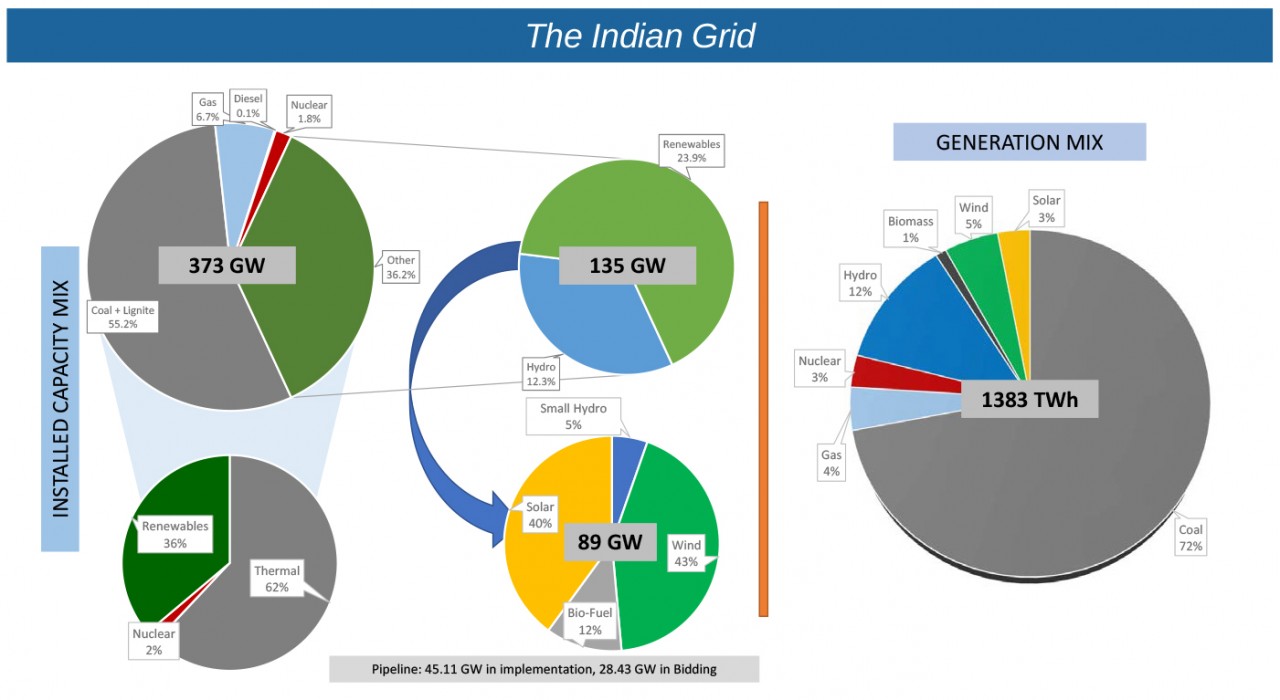

Renewable mix capacity

Over the past five years, India saw tremendous growth in renewables in addition to the grid (51 GW between 2015 and 2020). The maximum yearly addition was seen in 2017 (37 percent YOY growth), but ever since the year-on-year addition dropped, with only 4 percent growth YTD in 2020. This year, in spite of the disruptions propping up due to COVID-19 pandemic, we witnessed India's renewable capacity installation reaching 89.3 GW with wind being the major contributor with 43 percent share in the total renewable mix, followed by solar with 40 percent. As of October 31, 2020, about 36 GW (2 GW increase from 2019 levels) of solar and 38 GW (1 GW increase from 2019) of wind capacity is installed in India. The current pipeline of solar, wind and hybrid projects stand at 49 GW (in various stages of implementation) and 27 GW in various stages of bidding. This year also saw many enablers being brought to the table, from competitive bidding guidelines for renewables with thermal (which recently got amended to renewables complimented with any other source of power or storage), to RE hybrid bidding guidelines. Earlier in the year, during the budgetary session, energy storage was declared as the 'Champion Sector', and most recently, the government came out with a production-linked incentive of `18,100 crore for Advanced Cell Chemistry (ACC) battery manufacturing in India with a total subsidy to 50 GWh capacity till 2025. With the mission of making India self-reliant (Atmanirbhar Bharat), the government also increased custom duties on imports to encourage domestic manufacturing.

ES capacity & projects

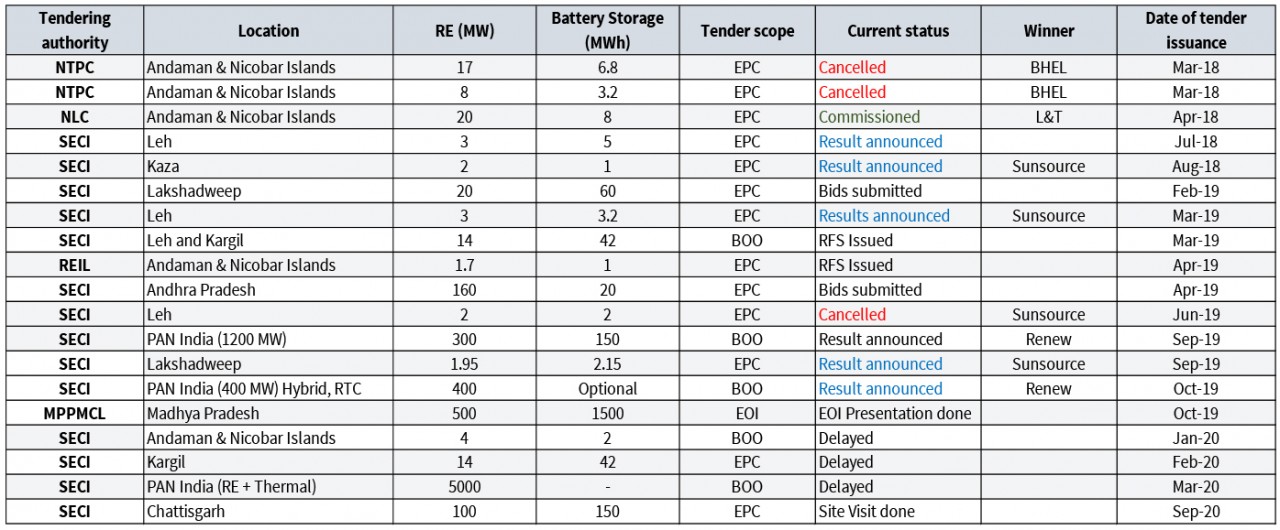

There were also new tenders which were introduced from renewable hybrids with storage (SECI 1.2 GW peaking tender) to RTC tender (SECI 400 MW RTC tender) to RE + thermal tender (SECI, 5000 MW tender) to many small-scale solar with storage tenders mainly for remote areas like Leh, Ladakh, Chhattisgarh, Lakshadweep, Andaman and Nicobar Islands.

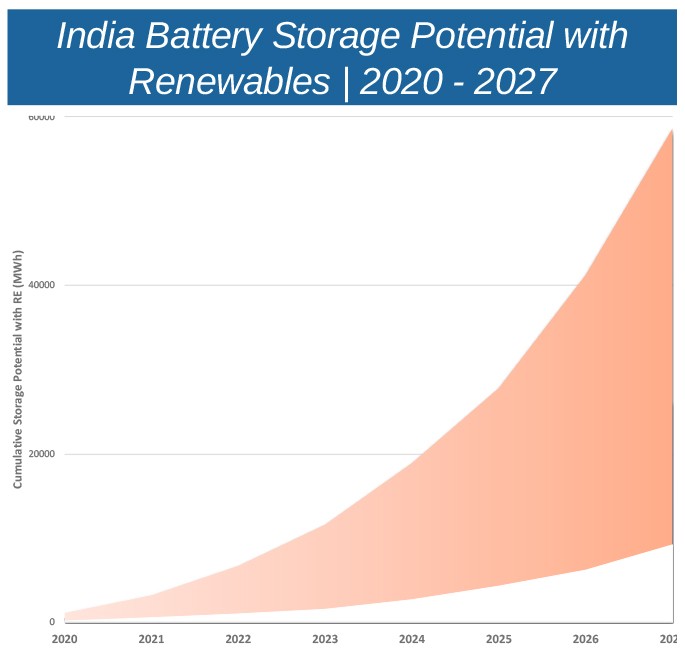

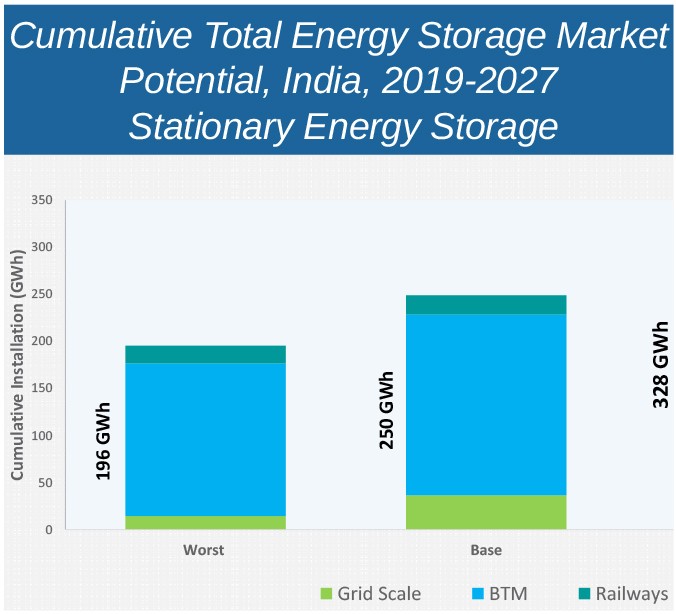

All these have in some way made the industry believe in the potential that energy storage holds for India in days to come with NITI Aayog itself seeing requirement of 630 GWh of storage capacity in India by 2030. IESA's projections (IESA Annual Energy Storage Market Overview) indicate a capacity of 328 GWh for stationary side only by 2027, with an increasing pie of renewable penetration in the same (74 GWh by 2027). Recent International Energy Agency (IEA) projections indicate that India will be the leader in installed energy storage capacity by 2040.

Looking at the targets that India has put forward of having a grid with 450 GW of renewables, Central Electricity Authority (CEA) projects requirement of 108 GWh of storage capacity at the generation-side by 2030 to effectively manage the transition. So overall, the present decade is set to be ruled by energy storage, which in turn will help the world make the shift towards a greener space through sustainably growing renewables.

Global ES scenario

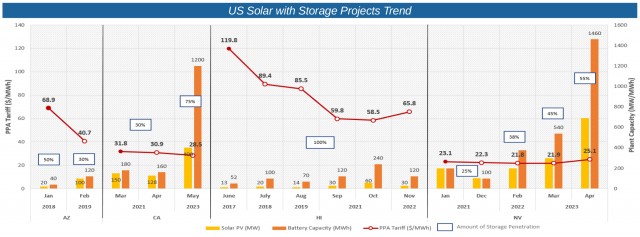

Looking at the world and the announcements being made globally; it just indicates the fact that storage is indeed the future of a renewable-heavy grid. According to Wood Mackenzie and the US Energy Storage Association's (ESA) latest 'US Energy Storage Monitor', 168 MW were deployed in Q2 2020 in the US. This is an increase of 72 percent quarter-over-quarter, 117 percent year-over-year and is the second-highest quarterly total ever seen, falling just behind Q4 2019 (186.4 MW).

The PPA prices for solar with storage projects also saw a decline of 16 percent in just one year, that too, with increasing penetration of storage in each new tender. Over and above, that 30 percent of all new projects in queue for approval in US are solar with storage projects which goes to show the development happening in the market. With each new tender and announcement, the size of such projects continues to grow bigger. Let us, therefore, look at the announcements.

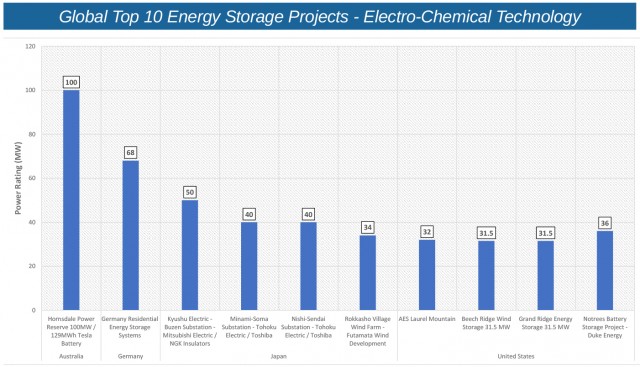

At present the largest RE + storage project is in Australia, the Hornsdale Power Reserve Project of 100 MW capacity for 1.28 hrs. The same is now also approved for expansion (150 MW/192 MWh). French renewable energy developer Neoen has won a contract with the Victoria government to the build the biggest battery in Australia in Geelong, providing essential services to the Victoria grid. The 300MW/459MWh Victoria big battery will be more than twice the size of the 150MW/194MWh Hornsdale Power Reserve, which was recently expanded to add new synthetic inertia and other key grid services to South Australia.

When you talk of growth you cannot forget China. China is building the largest vanadium flow battery in the world with a 200MW/800MWh capacity. It is being developed by Rongke Power Co. Ltd. and UniEnergy Technologies (UET). If the regulatory bodies give permission, in 2020, Strata Solar will build a 100MW/400MWh energy storage station in Oxnard, California. The project is expected to start in December and will be connected to the largest system of lithium-ion batteries in the world. Further, Pacific Gas & Electric (PG&E) have been granted permission from local regulator for construction of the largest battery system in the world. Its capacity will reach 567.5MW/2270MWh. The system will include four separate projects. The first one will be built by Vistra Corporation at the existing power station and have the capacity of 300MW/1200MWh. The other project built by Tesla and operated by PG&E will provide 182.5MW/730MWh from the local substation. All projects are expected to be commissioned by the end of 2020. They will replace three peak gas-powered stations. Finally, on October 15, a coalition of community-choice aggregators in California released the first major request for proposal targeting long-duration projects. To qualify, plants must be: 50MW or greater, able to discharge electrons at that level for eight hours or more, and should be in operation by 2026.

What about India? Well, we did progress as detailed before the tendering activity took place, we saw the NLC project in Andaman and Nicobar islands getting commissioned during the year (20 MW solar with 8 MWh of BESS), this was the second large scale storage project (first being the 10 MW/10 MWh Delhi AES – Tata Power Project) and the first of RE + storage project in India.

The year of promise

The year 2020 seems to have served as the foundation year where the required guidelines and policies have been laid out, it is time for the investors to now join the race. The guidelines are becoming increasingly specific; just to give an example, the recent RE Hybrid guideline, focuses on strict adherence to project delivery, monitoring and increased percentage of mixing (one of the two resources, i.e. wind and solar has to be 33 percent of the total capacity, this was 25 percent initially). The guideline now also allows for sale of excess energy to the market and talks about indexation of tariff. The guideline also specifies the minimal utilization requirement for such projects being 30 percent. Seeing the RE + thermal guideline which is now modified to RE + any source of power, the penalties for not meeting target of 85 percent availability is now raised to 400 percent of shortfall from initially being just 25 percent.

The sourcing of power for this guideline is now extended to any form of power along with renewables, where the percentage of renewables in the total mix must be 51 percent in terms of energy. All this looks quite promising, and in the true sense it is, but there are challenges too. As on date, around 20 GW of RE tenders that have already been awarded have not found a buyer, the effect of the same was noticed in the guideline where MNRE now has explicitly mentioned that six months post awarding of project if a power sale agreement (PSA) is not signed, the project will stand canceled.

The poor financial health of Discoms is a story well known (as on September, the total due was `1,30,452 crore). With each new RE tender, a lower tariff is realized, with `2.36/kWh being realized for solar this year, even during COVID times. Thus, Discoms do not want to buy or come into agreement with a project selling power at higher price. The Solar Energy Corporation of India (SECI) came out with the concept of pooling prices over a period and offering the same to Discoms to reduce higher price contract risks. Now, imagine the paradox; the 1.2GW SECI peaking tender was won by ReNew Power at a weighted tariff of `4.3/kWh and the same would supply power during peak times through BESS at `6.8/kWh. Post that the 400 MW RTC tender was again won at a first-year tariff of `2.9/kWh. Both these

prices surprised many in the industry as to how can power be supplied through BESS at such low prices. Yes, the prices are low, but not lower than what the Discoms are getting power at. Thus, till date SECI

has not been able to close the 1.2 GW peaking tender, even though it was awarded almost a year

ago now.

Discoms are not the only concern, there are other concerns too, like land clearances and clarity, in some of the RE+storage tenders there were disputes on ownership of project land which came up after the project was awarded. Sometimes due to land policy changes, developers face a lot of challenges in acquisition of land which results in delay of projects. Especially for RE Hybrids, getting such sites where both wind and solar resources are high is very challenging. Thus, the co-located tag that was there in the initial RE Hybrid policy, that came in 2018 was worrying, the same is now made optional.

What also has not helped India much specially in the present condition is non-availability of local manufacturing capacity and reliance on imports. This has led to further delay in project completions. Overall, there are a few challenges which need to be addressed quickly if we want this sector to grow and emerge as a market leader. SECI in the concept paper on high dispatchable renewables illustrated earmarking 120 GW of project capacity from the 450 GW of RE target by 2030 in innovative tendering section (40 GW – RTC, 40 GW – peaking power and 40 GW from flexible RE). This will aid in making the target of 450 GW of renewables more sustainable and reduce loss of increasing chances of RE curtailment, which almost looks unstoppable in a grid devoid of storage.

Invest, act and implement

To take control of this opportunity, which is knocking at our door, any delay in addressing will only increase the potential of India losing one more bus in the journey of energy transition. Well, the good news is, there are things happening in the right direction from all corners to make this work.

To begin with, there is the manufacturing program which is now approved by the Cabinet. The sooner this gets on ground the better as this will help in faster deployment, and India attaining the benefits of economies of scale. What can also help is having yearly targets for storage deployment (standalone and RE coupled) along with maybe having RPO like targets for storage too. The biggest benefit that storage bring is stacking of benefits and thus bringing in multiple revenue streams from a single deployment. This will need opening of the ancillary market for India, which today is quite restricted.

With deviation settlement mechanism penalties becoming stricter there are increased business cases for energy storage. As far as delay in signing PSAs are concerned, it would be a good move to have Discoms party to the process right from the planning stage to at first understand their requirement rather than entrusting them with new projects. This way, the delays in signing PSAs would reduce. One way of doing this is to have a yearly plan of energy demand requirement from the Discoms so that we target the lowest hanging fruit first. It's always great to achieve targets on time, but let us be sustainable in the race to achieve them, else a poorly planned RE heavy grid will only result in more challenges than yielding benefits.

There have also been studies that indicate that if there would have been storage deployment in the Mumbai grid, the blackout that happened recently in the financial capital of India could have been avoided. As the question is raised, how much cost will the installation incur? The answer to that is, what was the cost incurred due to the blackout? What is required is to see the story in its entirety than a piecemeal manner. Till the time we try to target one application through storage it will not look profitable, BESS installations will only make sense when we utilize the asset to its full potential and thus give rise to multiple benefit streams. While we need many more RE + storage projects we also need more like the 10 MWh project that we have in Delhi. In fact, a study by IFC projects a requirement of 100 MWh battery storage just in Delhi, thus imagine its potential at pan-India level.

One would tend to agree with a quote heard at a panel discussion recently: "Rather than thinking of mistakes which could be committed by doing a project with storage now, maybe it will be better to think about the mistakes and opportunities we are already missing by not doing a project now, lets look at leading indicators rather than focussing only on lagging indicators."

All in all, it is a great time to be in this sector, which never lets you be complacent and changes and innovates every day. What we will need to do is to start execution now, a lot of planning has already been done, a lot of discussions have already been heard, a lot of white papers written, a lot of presentations given and a lot many studies done and with several pilots and demonstration projects done too.

It is time we talk about project executions now and build the portfolio of storage projects. The article started off by saying that 2020 looks like the perfect foundation laying year where all ingredients are already in place from policy to guidelines, tenders to incentives, and it is now time to act. If we keep waiting for the technologies to get more efficient and the prices to drop further, which eventually will, the only problem is, we may end up missing out on another landmark opportunity knocking on our door.

Spotlight