MENA: Clean energy transition in top gear

Middle East and North African countries are diversifying their economies towards clean energy. Strategic plans are in place to boost renewable energy capacities, EV adoption, and green hydrogen production, supported by battery energy storage for grid integration and micro-grids, EV charging infrastructure, and export hubs for hydrogen, representing a significant opportunity like never before.

In the emerging race for decarbonization and sustainability, stakes are higher for nations and businesses across the globe. Pressures are mounting on all quarters to come clean; it's a "do or die" situation for all of them to stay relevant and afloat in the sweeping wave of clean energy pursuits.

For the Middle East and North Africa (MENA), the region quintessentially associated with the prosperity out of oil and gas exports for decades, the clean energy conundrum is being unraveled in a rather interesting way. Growing population and industrial expansion is mounting immense pressure on the existing energy infrastructure in the region, warranting large-scale investments for capacity addition.

Moreover, the livelihoods of over half a billion population in the region are under serious threat, thanks to the impact of climate change by way of severe droughts and rising temperatures, while the business and fiscal sustainability of companies and governments fully dependent on the oil industry is heading towards an imminent impasse.

Countries in the MENA region, therefore, are being forced to accelerate clean energy developments and diversify their economies to sustain the emerging global way of energy transition. Having said that, much to everyone's surprise, the region is standing up to the situation by finding innovative means and new pathways to embrace clean energy technologies in recent years.

Efforts are on to leverage the geographical and strategic advantages for efficient renewable energy (RE) generation and consumption in local energy markets and applications, while also exhibiting the entrepreneurial spirit of the region by enabling energy exports to strategic global markets.

On the whole, the MENA region's hold on the global energy sector is far from over and is now branching into new avenues. This special feature of ETN brings a snapshot of what the region stands for in the emerging clean energy transition, by taking stock of the megatrends and latest developments in three specific areas, namely, energy storage, e-mobility, and green hydrogen.

Energy Storage

Clean energy transition begins with efficient integration of variable RE sources into the power grid. Energy storage systems (ESS) play a cardinal role in this aspect, since ESS deployment is the only solution to overcoming the intermittencies of renewable energy. ESS helps to smoothen power output by storing excess power during off-peak hours and releasing it during peak hours or as per requirement.

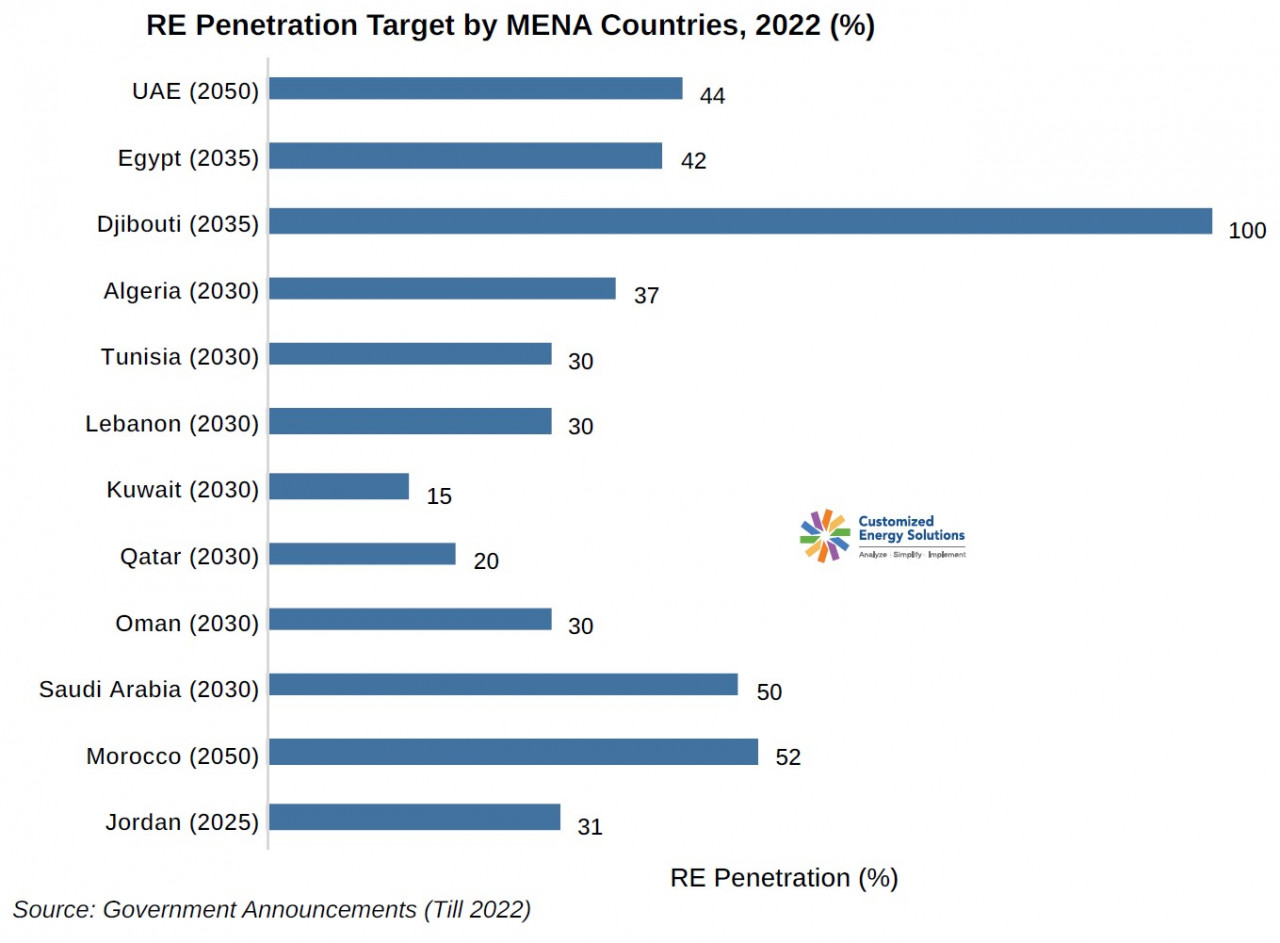

Claimed as one of the most potential regions for RE and energy storage in the world, the MENA region has just began exploring its potential and unlocking the region's natural and geo-political advantages in this area. Storage projects are becoming key factors in achieving RE targets in the region, especially in countries such as Jordon, Israel, Morocco, the UAE, Saudi Arabia, Egypt and Oman.

According to CES's MENA Energy Transition Outlook (November 2023), about 40 to 50 GWh of ESS is expected to be deployed in the region till 2030, to manage variable RE projects for optimizing the grid to meet the current renewable energy targets set by the nations.

A fair share of ESS projects, both planned and already operational, are being readied across the GCC (UAE, Saudi Arabia, Qatar, Oman) and North Africa (Egypt, Morocco, Algeria and Tunisia), while some key projects are under way in the Levant (Jordan, Iraq and Lebanon).

The focus is more on grid-scale and RE-plus-storage. Targeted applications include frequency regulation, capacity firming, peak shaving, wholesale price arbitrage, and captive use. Replacement of diesel gensets with BESS, especially battery-based solutions, for heating, ventilation and air-conditioning (HVAC) and backup power is also aspired for.

COP28: GEAPP's multilateral consortium targets 5GW of battery storage by 2024

Pumped hydro storage (PHS) and electrochemical energy storage, Sodium-Sulphur (NaS) and lithium-ion batteries in particular, are the preferred technologies in the region. The storage duration hovers between 32 minutes and 2 hours for li-Ion batteries, 6 hours for NaS batteries, and 10 hours in the case of thermal storage.

This year saw the maximum momentum for advanced ESS in the MENA region. Some of the latest developments are as following:

- Senegal's national utility Senelec has recently signed a 20-year CCA for a 40 MW/ 160 MWh (4-hour) BESS project with Infinity Power.

- Israel has announced 800 MW/ 3,200 MWh BESS buildout comprising four facilities of 200 MW and 4 hours' storage duration each in the northern Gilboa mountain range region.

- West Africa's first BESS project (16 MW of solar PV with 10 MW/ 20 MWh) dedicated to frequency regulation is coming up in Senegal – the largest BESS in the country as of now.

- Masen is undertaking Noor Midelt III solar-storage project with 400 MWh of BESS capacity in Morocco – the largest energy storage project in the country.

- Ncondezi Energy has secured land agreement for 300 MW solar-cum-storage project in Mozambique early this year.

- South Africa has floated an RfP for 513 MW of battery storage early this year.

- Sungrow to build 536 MW/ 600 MWh BESS for ACWA Power in Neom smart city in Saudi Arabia.

- Emirates Water and Electricity Company (EWEC) has called for 300 MW/ 300 MWh of BESS capacity in UAE in the next three years. Later, in September 2023, EWEC floated an expression of interest for 400 MWh battery storage project meant for grid services.

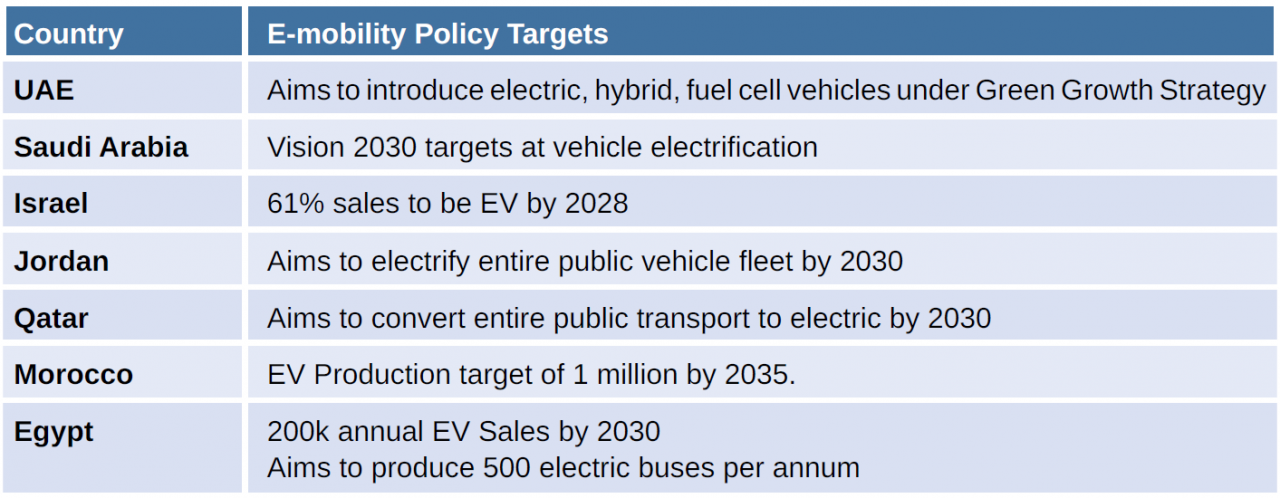

E-mobility

In 2021, transportation accounted for about 28 percent of CO2 emissions in the MENA region, according to research estimates. Concerted efforts by governments and other stakeholders are in place to decarbonize the sector through electric mobility, despite the advantages of cheaper oil that continues to play spoil sport for clean mobility in the region.

Leading countries in this emerging e-mobility scenario are Turkey, Israel, Jordon, UAE, South Africa, Saudi Arabia, and Egypt. Governments have already announced their national EV adoption targets, while private investors are identifying unique opportunities to capitalize in the EV space, which is seen as a corollary to the emergence of RE, energy storage, and smart grid initiatives in recent times.

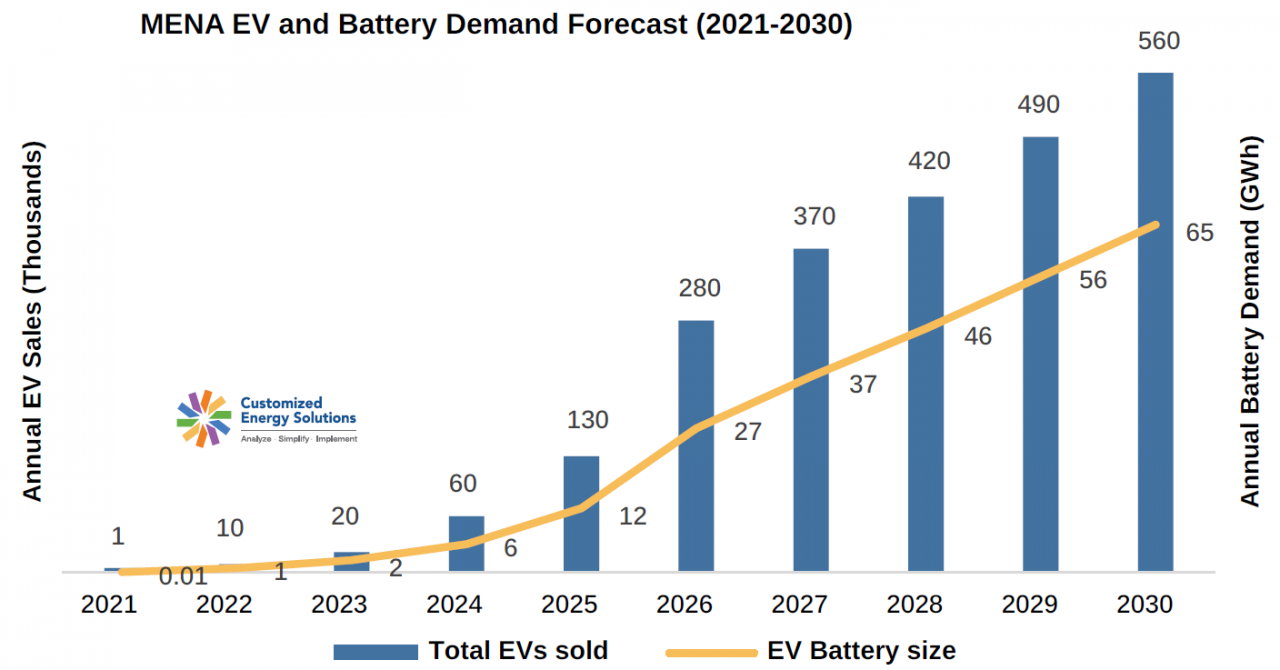

A forecast from CES opines that annual EV demand in the region would cross 130,000 units by 2025 and 560,000 units by 2030, considering national targets and current EV sales trend in these countries.

As a corollary to emerging demand for electrification of public transport, commercial fleet and private vehicles in the MENA region, the demand for batteries is also expected to increase significantly. The annual battery demand for new vehicles is estimated to grow from ~12 GWh in 2025 to ~65 GWh in 2030, according to CES's MENA Energy Transition Outlook (November 2023).

In this backdrop, here are some of the key developments in the e-mobility and EV adoption scenario in the region:

- UAE has revised its national EV policy with a target of achieving 50 percent EV penetration in total vehicle parc by 2050. The country also plans to build 914 AC and DC charging stations for electric vehicles by the end of 2023.

- The country's target is to establish 30,000 chargers by the end of 2050, when the share of electric and hybrid vehicles will be 53 percent of the total vehicle parc.

- Abu Dhabi National Oil Company and Abu Dhabi National Energy Company have established a JV 'E2GO' to build and operate EV charging infrastructure across the UAE.

- Dubai has vowed to increase the city's network of public charging stations by 170 percent over the next three years – from 370 points currently to 680 by 2025.

- Dubai Electricity & Water Authority has set a target to have more than 1,000 public charging stations by 2025 across Dubai.

- Saudi Arabia has set a target of deploying 34,000 public charging stations in the country by 2030. The state-owned Public Investment Fund (PIF) is deploying action plans to develop a robust ecosystem for EV charging infrastructure and related services in the country.

- Israel has registered a 10 percent rise in EV sales in the first half of 2023 as against last year.

- Turkey is fast emerging as an EV manufacturing hub in the Middle East, with global OEMs such as Ford, Toyota, Hyundai, and Renault establishing JVs for EV assembly to cater to local and export markets.

- ABB is working on an EV charging infrastructure development contract to deploy public chargers at multiple locations in Qatar since 2021.

Green Hydrogen

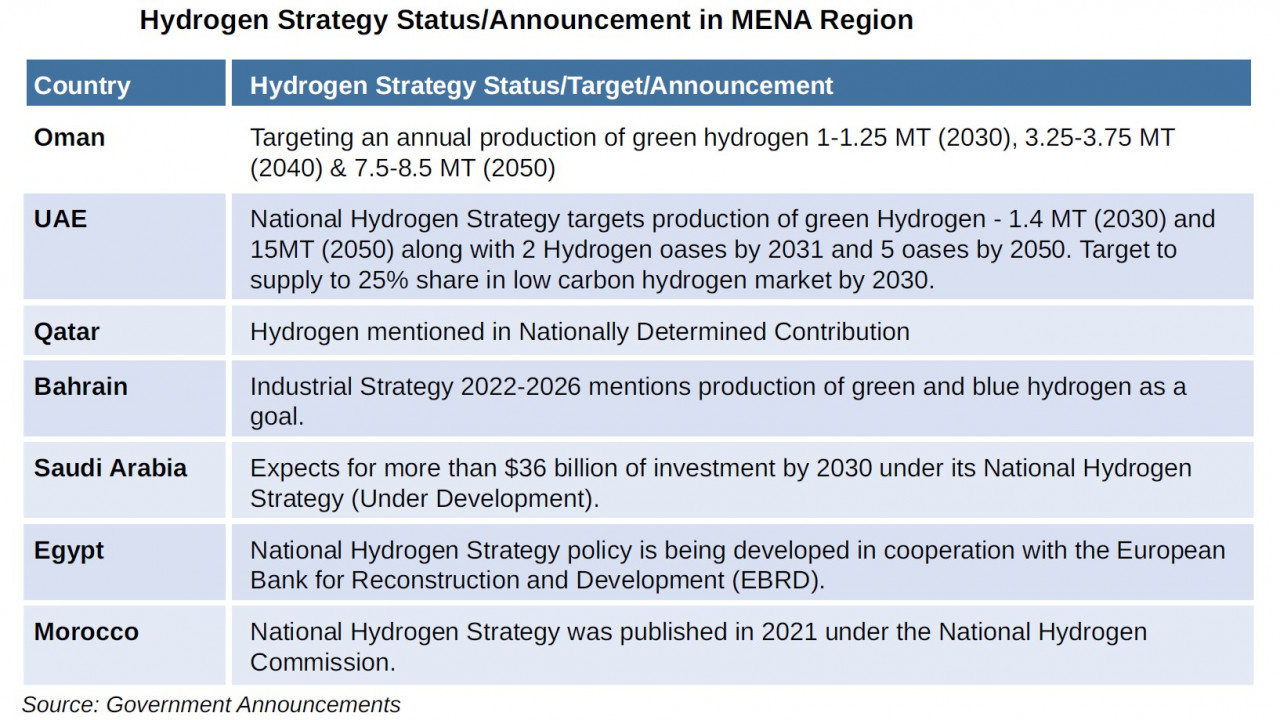

Renewable hydrogen is at the forefront of MENA region's clean energy and sustainable future. The region is under the spotlight for significant green hydrogen-related strategic national plans and investments in recent times, especially since COP27 held in Egypt last year, now furthered by COP28 in the UAE in December.

Thanks to a combination of factors such as rising global demand (especially from Europe), cost reductions via innovation, and pre-existing conditions suitable for production (including affordable RE and transportation of green hydrogen), the region is emerging as a robust hydrogen export hub catering to the global supply chain for renewable hydrogen in the coming decades.

MENA region currently accounts for about 10 percent of hydrogen production globally, although most of it is gray hydrogen made from fossil-based energy sources. By 2050, the region is expected to double its global share to around 20 percent, with blue hydrogen (using methane and carbon-capture) and green hydrogen dominating.

Egypt enacts law to offer up to 55% tax credit, non-tax incentives for H2 projects

At present, over 46 green hydrogen and ammonia projects have been identified across the Middle East and Africa, with an estimated total budget of more than $92 billion. Although the current active hydrogen capacity is just 0.2 million tonnes per annum, reports predict a huge capacity expansion in the coming years owing to higher export potential.

Countries such as Egypt, Mauritania, Morocco, Oman, Kenya, the UAE, South Africa, Namibia, Qatar, Saudi Arabia, and Bahrain are taking the lead in the emerging hydrogen ecosystem in the MENA region. Efforts are on to establish multiple production and storage centers, including port-based export hubs and pipeline networks for Europe and Asia.

Egypt, for instance, is currently sitting on a pipeline of green hydrogen and green ammonia investments worth $83 billion from various international developers, with over 20 MoUs on the anvil to make the country a hydrogen hub in the MENA region.

Technology wise, the high temperature variant of Proton Exchange Membrane (PEM) and Solid Oxide Electrolyzers Cell (SOEC) that split water into hydrogen and oxygen molecules are best suitable for MENA region due to their high ambient temperature operation, according to the CES's MENA Energy Transition Outlook (November 2023).

Further, the region's advantage of being able to produce blue hydrogen using natural gas (by steam methane reformation) and carbon capture cannot be overlooked. Thanks to the abundance of cheap natural gas, blue hydrogen is also considered as an attractive option for the MENA region. Although not completely sustainable as green hydrogen, blue hydrogen can still be an effective carbon-neutral option for kick-starting the hydrogen economy in the immediate to mid-term phase of energy transition.

Some of the latest developments in MENA's green hydrogen landscape are as following:

- At COP27, Egypt garnered nine projects worth $83 billion, having a combined capacity of 7.6 million tonnes of green ammonia and 2.7 million tonnes of green hydrogen per year.

- UAE has announced two hydrogen production hubs called as 'oasis' by 2031, with a production target of 1.4 million tonnes of green hydrogen per year by 2031 and 15 million tonnes by 2050.

- Saudi Arabia's NEOM Helios – claimed as the world's largest green hydrogen plant – has concluded EPC agreements with Air Products and other agreements with financial institutions. The project is under construction and scheduled to become operational in 2026.

- About 4 GW of solar and wind capacity and ESS are envisaged to produce 600 tonnes of green hydrogen per day and 1.2 million tonnes of green ammonia annually.

- In Oman, Acme Group's green hydrogen hub with capacity to produce 2,400 tonnes per day of green ammonia for an annual production of 0.9 million tonnes became operational.

- ACWA Power, OQ, and Air Products have invested in a green hydrogen-based ammonia plant in Oman. Preliminary works for construction of the facility have begun.

- Marubeni Corporation and Saudi Arabia's PIF are conducting a feasibility study for producing clean hydrogen in the country for export markets. PIF is already working on another green hydrogen project with POSCO, finalized in 2021.

- Hyphen Hydrogen Energy has announced the next phase of a $10 billion green hydrogen project coming up in Namibia.

- German Moroccan Energy Partnership for joint development of green hydrogen production has invested €300 million to export green hydrogen from Morocco to Germany in the coming years.

- Omani OQ, EnerTech, and InterContinental Energy are together developing 25 GW of RE for green hydrogen and ammonia production, with exports expected to commence through Duqm port from 2028.

The MENA region has been one of the fastest growing regions over the past decade and there is a pathway for the region to position itself at the forefront of sustainability efforts while maintaining its upward economic trajectory. As global markets continue to shift, and energy demands rise, the region requires bold and coordinated action from policy-makers and businesses to lead a just energy transition and meet both climate- and development-related goals"

Børge Brende, President, World Economic Forum.

On the whole, the MENA region is up for a massive transformation like never before. Not just in terms of its energy transition, but also in engendering sustainability in its economies and well-being of its population. However, this transition is a long-term process that warrants broad-ranging programs cutting across the different work streams and coordination among various stakeholders.

Successful realization of national energy transition plans will largely hinge on long-term planning and bold measures from policymakers and private players, supported by multi-stakeholder partnerships for robust technologies and finance. With strong economic diversification, skilling of resources for green jobs and vibrant leadership, the MENA region will soon be at the heart of the global energy transition.

* With inputs from Customized Energy Solution's (CES) MENA Energy Transition Outlook (November 2023)

MENA: Top 6 'high-potential' countries for low-carbon hydrogen