IESA ranking of ES companies in India for 2020

IESA has initiated a new research program to benchmark energy storage and EV companies across various application segments in India. This ranking aims to identify the top players in the market and showcase exemplary performance and practices.

Electric mobility and stationary storage markets have been in the limelight during this year. The National Mission of Transformative Mobility and Battery Storage that was announced in 2019, and the National Programme for Advanced Chemistry Cell manufacturing in 2020, have given major impetus to the EV and stationary storage markets.

The government of India has set a vision to make the country a global hub of manufacturing of EVs in the next five years. To fulfil this vision and to create an ecosystem to accelerate the uptake of EVs in the country, the government has taken several policy initiatives with schemes like FAME-II scheme, NMTMBS, and announcing benefits like lowering the GST for EVs, making EV charging a service along with the recent acknowledgement of registration of EVs without batteries as a business model.

IESA's research program aims to identify the top players in the market, based on various criteria, namely -- market share, revenue and revenue growth rate, technological advancements, and export revenue. These criteria are constant across all the market applications.

This ranking practice is expected to bring in more transparency in the energy storage industry, which is fragmented across various segments. It is envisaged as a channel for the industry players to showcase their exemplary performances and best practices. Also, it helps the top players to benchmark their business performance with respect to the market.

Electric Vehicles

In the last couple of years, more than 100 companies have already entered the segment across the supply chain. Hence, to track the growth of the EV market in India, IESA has taken the initiative to benchmark EV companies present in various segments of the market. The the top companies are identified based on various criteria like, market share, revenue, sales growth, product portfolio, localization content, geographic presence, technology enhancements, innovative business models, etc. This initiative hopes to provide a platform for industry players to showcase their product/ service performance and best practices.

The major EV segments covered in the ranking exercise are e-2W, low- speed and high-speed e-3W, e-4W and e-buses. The following section discusses the market leaders in each segment based on research.

The e-2W segment has witnessed 21 percent growth in the last financial year. As per Society of Manufacturers of Electric Vehicles (SMEV), industry sold 1,52,000 units in 2019-20 as compared to 126,000 units in 2018-19. Low speed e-2Ws dominated the market despite subsidies being removed for this segment in FAME-II scheme.

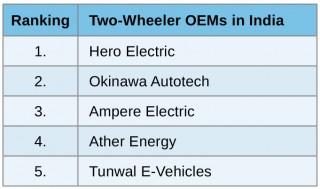

Considering all the ranking criteria, Hero Electric was ranked as the leader in this segment for FY 2019-20. The company has a share of 33 percent, and witnessed a growth of 34 percent in sales as compared to sales in 2018-19. Hero is currently having a network of 650+ dealers across the country and expects to increase it to 1,000 by end of this year. To address the issues related to range anxiety, the company is offering detachable Li-ion packs. Additionally, the company is also investing in creation of charging infrastructure for their customers. Going forward, Hero Electric is looking to focus more on entry level and city speed vehicles as a major market for them along with launch of performance vehicles for the high-speed segment.

Other companies in the ranking list are Okinawa, Ampere Electric, Ather Energy, Tunwal EVs, Jitendra New EV Tech and Revolt motors. Okinawa remained the market leader in the high-speed segment in the last financial year and sold over 10,000 units, the company also achieved over 85 percent localization. Ather Energy achieved localizing most of the components of the drive train except battery cells and controllers.

There have been many innovative solutions and business models that have emerged in this sector.Ampere Electric has recently introduced battery as a subscription model. Ather Energy has introduced buyback program for Ather 450. Hero Electric is offering e-scooters to the customer for few days to have an experience without any upfront cost; and Revolt motors is offering charged batteries to their customers at home.

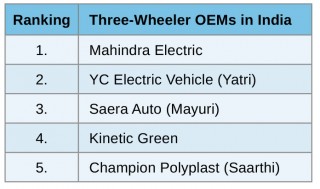

Low-speed Electric Three-Wheeler Segment (e-rickshaw)

The e-rickshaw market in India has evolved since 2013. As per ICAT, 600+ registered OEMs are present in the market. Apart from the registered OEMs, there is also a substantial grey market in this segment. As per CES research, the annual sales for this segment is between 2 to 2.2 lakh units for last financial year, considering 40 percent market with organized players and 60 percent with unorganized players.

Mahindra Electric was ranked as the leader in this segment for FY 2019-20. In terms of only sales units though, Yatri closed highest unit sales during the year. The market here is heavily dependent on imports, however, companies like Mahindra Electric and Kinetic Green have started domestic manufacturing of all their components, except the battery cells.

This segment has been predominantly dominated by lead-acid chemistry but transition to Li-ion is being observed

e.g. Kinetic Green and Mahindra Electric are selling more e-3Ws with Li-ion batteries. Saera Electric has the highest number of dealers (250+) in India, followed by Mahindra and Kinetic Green.

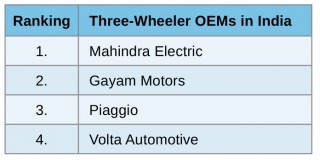

High-speed Electric Three-Wheeler (L5 e-Auto) Segment

The high-speed e-auto market in India has slowly started gaining momentum. The market has opened mainly at B2B level and in the cargo segment. As per CES research, industry sold 5,000 units in the last financial year.

Considering all the ranking criteria, Mahindra Electric was ranked as the leader in this segment for FY 2019-20. The company enjoys a market share of 80 percent followed by Gayam Motors, that has a share of ~15 percent. Mahindra also has been proactive in localizing its component-level production through the years and enjoys a much broader presence across India.

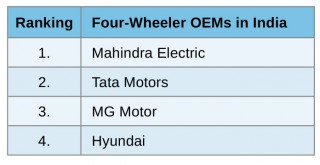

Electric Four-Wheeler (E-4W) Segment

The e-4W car market is at a nascent stage. The share of e-cars in the personal segment has increased gradually over the years. As per CES research, industry sold ~3,000 units in last financial year.

Mahindra Electric was ranked as the leader in this segment for FY 2019-20. Mahindra Electric enjoys ~45 percent of market share followed by Tata Motors with a share of ~34 percent. Mahindra offers cars across 50 cities with over 65 dealership, Tata Motors offers Tigor in 30 cities and Nexon EV in 22 cities, MG Motor in 10 cities, and Hyundai in 30 cities. The market has gained traction from the customers with the launch of new high performance models. MG Motor received over 3,000 bookings within one month and Nexon EV has outperformed other models and is dominating the market in 2020.

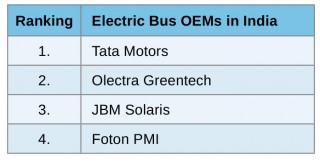

Electric Bus Segment

The e-bus market has started to gain momentum with subsidy support from the government. Majorly pilot projects were carried out so far across different cities. In the last financial year, industry sold nearly 500 units.

Disclaimer: FAME-II orders have not been considered to estimate the market share as the tendering process is still underway.

Considering all the ranking criteria, Tata motors was ranked as the leader in this segment for FY 2019-20. The company enjoyed a market share of ~59 percent followed by Olectra with a share of ~31 percent.

Tata motors won the single largest tender of 300 e-buses from Ahmedabad Janmarg and Olectra won the tender to supply 150 e-buses to PMPML, Pune. Based on pilot projects and trials carried out, Olectra has deployed buses in six cities and completed trials in ~15 cities across the country. Tata also deployed 255 buses in six different cities under FAME-I and carried out trials in States like Maharashtra, Himachal, Assam, and Chandigarh.

Stationary Energy Storage

Major market segments covered in the stationary storage markets are behind-the-meter (BTM) applications namely - inverter back-up, telecom tower backup, UPS back-up and solar rooftop. IESA aims to cover other categories such as energy storage companies in utility-scale applications, EVs, etc., in the subsequent editions of the ranking list.

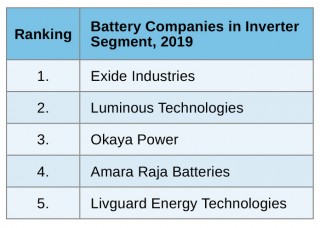

Energy Storage Companies in Inverter-back-up Application

With India witnessing a significantly lower frequency of power cuts in 2019 as compared to 2018, and the years prior, the power reliability has improved and led to a lower dependence on inverters. This development brought down the demand for batteries for inverter backup and was reflected in the shrinking market for the same. The total inverter battery backup market size stood at 12.7GWh as on 2019.

This segment is still dominated by the lead-acid batteries. In 2019, Exide remained the market leader with revenue share of 27 percent (in the organized sector). This market segment is highly fragmented with numerous players in the SME and unorganized segments. Since the introduction of GST in 2018, the share of the market in unorganized players has been shrinking significantly, from 55 percent in 2018 to 45 percent in 2019 and currently at 32 percent. Exide, the market leader has been successful by introducing price competitive products to compete with the local brands. Exide and Luminous together formed 50 percent of the market share in 2019. Luminous is one of the few players in India to have forayed into Li-ion-based inverter battery backup solutions, with its Luminous Regalia, coming with a battery warranty of five years.

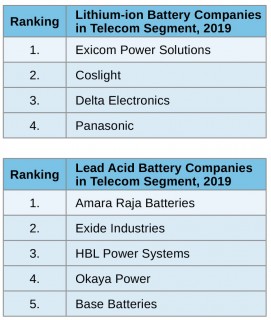

Energy Storage Companies in Telecom sector

The energy storage market for telecom witnessed a stable growth in 2019, with the market size standing at 2.2GWh.

In the lead-acid battery segment, which constituted 80 percent of the MWh share in telecom in 2019, Amara Raja is the market leader. Along with its high market share, Amara Raja scores high in terms of technological advancement and its exports. These are the main reasons for its status as the leader in lead-acid batteries in the telecom sector.

Li-ion batteries constituted 20 percent of the MWh share in the telecom segment in 2019. In the Li-ion chemistry, Exicom was the market leader, and held 60 percent market share in 2019. Their strong client relationship with telecom tower companies, especially that with the largest consumer of this chemistry in the segment has helped them gain repeated business from the customers. Moreover, their strong R&D capabilities for product customization has been a major factor for their healthy growth in the telecom market.

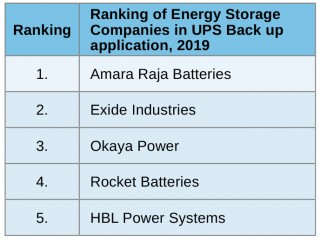

Energy Storage Companies in UPS back up Applications

With the demand for UPS growing sharply in manufacturing, healthcare, IT and datacentres, the UPS backup market witnessed a growth rate of 9 percent in 2019 and stood at a market size of 3.1GWh. The highest demand for UPS is expected from the healthcare and datacentre applications, potentially giving rise to higher demand of UPS backup market in these segments.

Amara Raja is the market leader in the batteries for UPS back up market segment with market share of nearly 35 percent. Their major strengths include extended warranty batteries, competitive pricing, and franchisee–based distribution model. IESA also gives Amara Raja a good score on export revenues and growth rate. These factors make Amara Raja the clear topper in the Ranking List of companies in UPS segment.

Following close on its heels is Exide, which offers strong technology upgrades to extend the battery life. The company also uses recyclable lead for its batteries, because of which it is less exposed to lead price fluctuations. The combined presence of Exide and Amara Raja accounts for a market share of 67 percent in the UPS backup market in 2019.

Energy Storage Companies in Solar Rooftop Applications

The solar rooftop segment is the fastest growing energy storage segment in the BTM market and grew twice the potential from 2018 in 2019 – a possible result of the lowering of GST to 5 percent on solar batteries. In 2019, the market size for solar rooftop batteries stood at 200MWh (or 0.2 GWh).

Exide Technologies led the market with 23 percent market share in 2019. Exide's export revenue has been increasing significantly in this space due to the organisation's entry into partnerships with countries in Southeast Asia and Middle East. Moreover, the strong network of more than 36,000 outlets and service centres is a major strength of the company which aid their leadership position in the inverter and solar applications.

(Disclaimer - The scores are based on data collected mainly through primary interviews, and public databases such as Vahan portal.)

Spotlight