The pathway to decarbonization through energy transition

The World Energy Transitions Outlook outlines a pathway for the world to achieve the Paris Agreement goals and halt the pace of climate change by transforming the global energy landscape. Gayathri Prakash and Ricardo Gorini of International Renewable Energy Agency (IRENA) discuss the key findings of the report and the steps towards accelerating global energy transition with Moulin Oza, Assistant Editor, ETN.

Please tell our readers about IRENA's World Energy Transitions Outlook: 1.5°C Pathway report. What are the key findings of the report?

IRENA's flagship publication "World Energy Transitions Outlook" outlines a pathway for the world to achieve the Paris Agreement goals and halt the pace of climate change by transforming the global energy landscape. This report presents options to limit global temperature rise to 1.5°C and bring CO2 emissions to net-zero by 2050, offering high-level insights on technology choices, investment needs, policy framework, and the socio-economic impacts of achieving a sustainable, resilient, and inclusive energy future.

Some of the key findings of the report include:

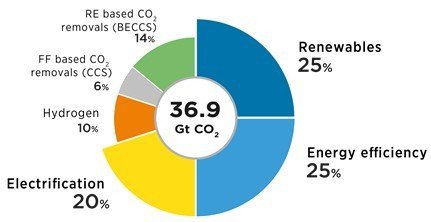

- Over 90 percent of the solutions shaping a successful outcome in 2050 involve renewable energy through direct supply, electrification, energy efficiency, green hydrogen, and bioenergy combined with carbon capture and storage (BECCS). Innovative solutions are reshaping the energy system. Yet, the necessary deployment levels at a speed compatible with 1.5°C will require targeted policies and measures.

- Energy sector investment will have to increase by 30 percent over planned investment to a total of $131 trillion between now and 2050. IRENA's analysis also shows that when the reduced externalities from lower air pollution and avoided climate change are combined, the overall benefit of the energy transition is valued at between $2 to $5.5 saved for every additional $1 spent. Sharp adjustments in capital flows and a reorientation of investments are necessary to align energy with a positive economic and environmental trajectory.

- A transformed energy sector will grow from 58 million in 2019 to 122 million jobs in 2050, renewable energy jobs alone will account for more than a third (from 11.5 million in 2019 to 43 million in 2050). A holistic global policy framework is needed to bring countries together to commit to a just transition that leaves no one behind and strengthens the international flow of finance, capacity, and technologies.

Please elaborate on the present pace of global energy transition. What kind of future steps will enhance the transition?

Key drivers such as climate change, energy security, energy access, and air pollution have placed a renewables-based energy transition at the forefront of the national, regional, and global agenda. Fortunately, renewables are increasingly the lowest-cost source of electricity in many markets, capping a remarkable decade of change for a renewables-based generation of electricity, during which the cost of utility-scale solar PV, for example, fell by 85 percent by 2020 compared to 2010 based on IRENA's renewables cost database. The momentum of renewable energy is further demonstrated by its resilience in the face of the COVID-19 pandemic.

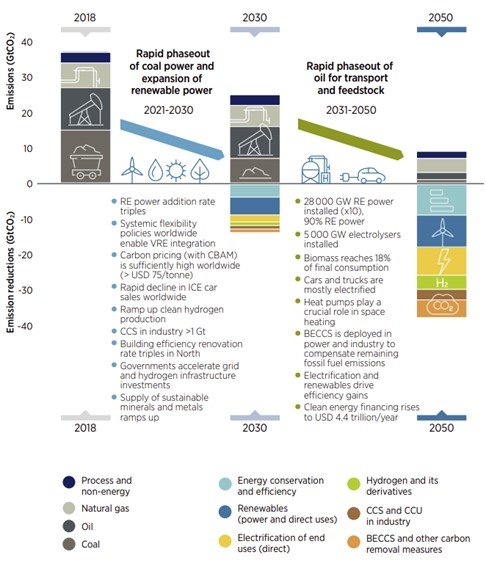

A record level of 260 gigawatts (GW) of renewables-based generation capacity was added globally in 2020, more than four times the capacity added from other sources. Trends to date have shown the way towards a decarbonized sector in 2050 but they have had little or no effect on rising emissions. Indeed, progress still falls woefully short of what is needed to hold the rise in global temperature to 1.5°C by 2050. The time dimension is crucial to realize such a massive transition and a radical shift is required on multiple fronts based on readily available renewable energy and energy efficiency technologies that can be scaled up now.

A net-zero carbon future by 2050 may seem a daunting challenge. But IRENA's analysis indicates that it is feasible. Achieving it will require a massive ramp-up of efforts on seven fronts:

- The rate of decline in energy intensity must move from the 1.2 percent recorded in recent years to three percent. Here, renewable power, electrification, and circular economy principles have key roles to play, as do conventional energy efficiency technologies.

- Annual growth in renewable energy's share in the globe's primary energy production needs to accelerate eight-fold from its share in recent years.

- Renewable power generation capacity must grow from over 2, 800 GW today to 27, 500 GW by 2050, or 840 GW per year, and a fourfold increase in the annual capacity additions have been recorded in recent years.

- Electric vehicle sales must grow from 4 percent of all vehicle sales today to 100 percent, with the stock of electric vehicles growing from 7 million in 2020 to 1.8 billion in 2050.

- Hydrogen demand must increase from 120 Mt to 614 Mt in 2050, a fivefold increase. The share of clean hydrogen in overall demand needs to grow from 2 percent to 100 percent. Two-thirds of demand would be met by green hydrogen; one-third by blue. Meeting that goal will require the addition of 160 GW of electrolysers each year between now and 2050, from the 2020 base of 0.3 GW of installed capacity.

- The total primary supply of biomass needed to achieve net-zero emissions by 2050 would be just over 150 EJ, a near tripling of primary biomass use in 2018. Based on a detailed assessment of the potential supply of sustainable biomass, this appears feasible.

- Carbon capture and storage must grow from 0.04 Gt captured in 2020 to 7-8 Gt in 2050, with BECCS accounting for half of the total amount captured and stored.

Investment is one of the key requisites for advancing global energy transition. What kind of investments can aid the process in your view?

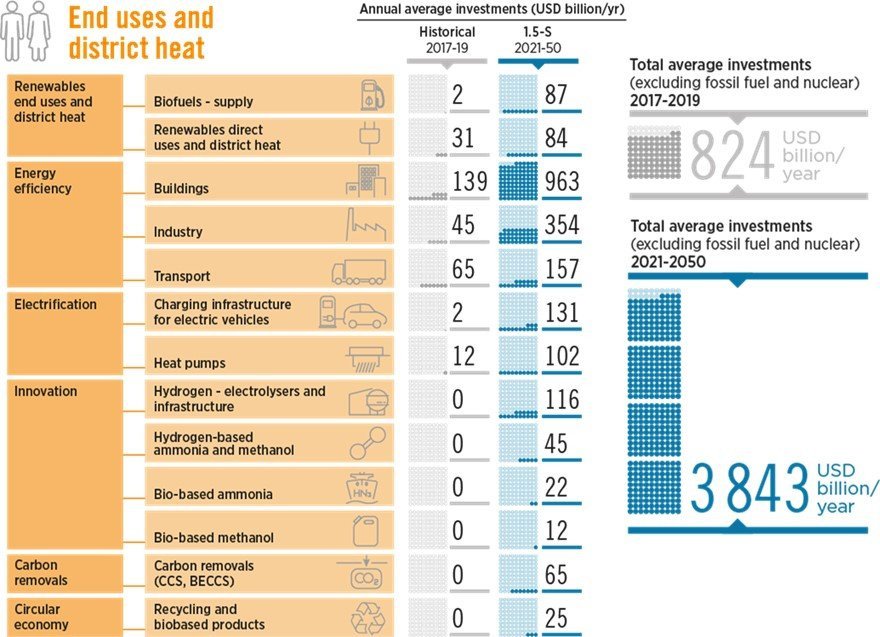

Ensuring a sustainable, climate-safe future calls for the scale-up of investment from the currently planned $98 trillion between 2021 and 2050 (under PES (Private Equity Scheme) to $131 trillion (under the 1.5°C Scenario) between now and 2050 – an incremental increase of 34 percent. The 1.5°C Scenario would require an additional $1.1 trillion per year over the PES, plus the redirection of investments from fossil fuels towards energy transition technologies (renewables, energy efficiency, and electrification of heat and transport).

High upfront investments are critical mainly to enable the accelerated deployment of key renewable energy technologies in the power sector; a massive scaling up of electrification of transport modes and heating applications, along with an expansion of accommodative infrastructure; and large-scale green hydrogen projects.

To highlight few investment opportunities:

- Investments in electrolyzers to produce green hydrogen, hydrogen supply infrastructure, and renewables-based hydrogen feedstocks for chemical production would exceed $160 billion per year on average through 2050.

- Bioenergy investments would rise to $226 billion per year (6 percent of total transition-related investment), most of which to increase the biofuels supply.

- Transport investments would rise to $375 billion per year (10 percent of total transition-related investment), excluding the incremental costs of electric vehicles.

- The average annual investment needed in the buildings sector ($1.09 trillion per year) is dominated by energy efficiency investment ($0.96 trillion per year); the remainder going for heat pumps and uses of other renewables, largely solar thermal.

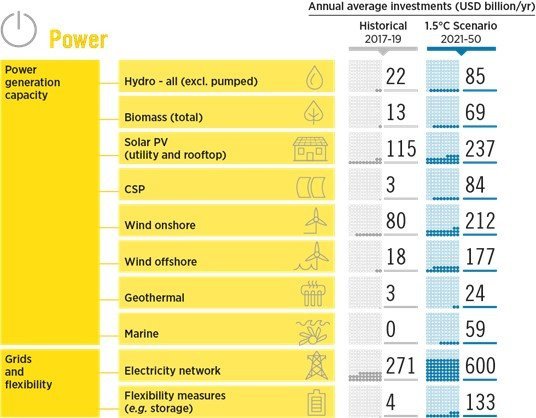

- In the power sector, accelerated investment of $1.7 billion per year would account for 44 percent of the total required energy transition investment over the period to 2050. Investments would be directed towards additional renewable power generation capacity, grid extension, and resiliency, and other grid flexibility measures (from better renewable power generation forecasting to integrated demand-side flexibility and stationary battery storage).

Advance energy storage technologies are the need of the hour. Please tell us about the kind of innovation required.

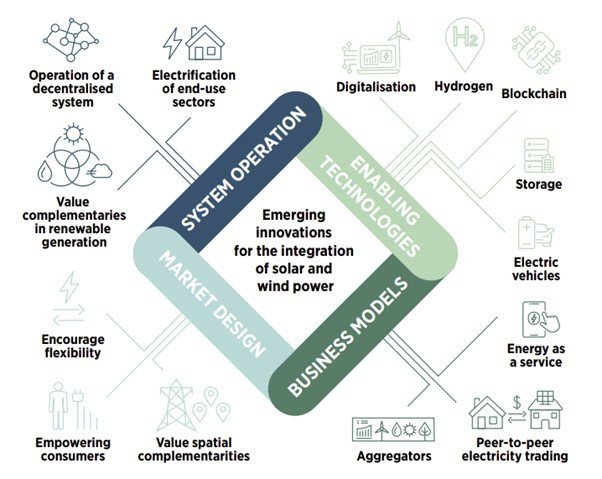

The flexibility of power systems is a key enabler for integrating rising shares of variable renewable energy (VRE) sources such as solar PV and wind. By 2050, 73 percent of the installed capacity and 63 percent of all electricity generation would come from variable resources (solar PV and wind), up from 15 percent of installed capacity and 7 percent of electricity generation in 2018. Such a level could be manageable with current technologies leveraged by further innovations.

On a technology level, both long- and short-term storage will be important for adding flexibility. The amount of stationary battery storage (which excludes electric vehicles) would need to expand from around 5 gigawatt-hours (GWh) in 2018 to over 16 000 GWh by 2050. When the battery storage available to the grid from electric vehicle fleets is included (assuming an approximate availability factor for arbitrage), this value will increase by over 25, 000 GWh to about 42, 000 GWh. The production of a very large volume of hydrogen from renewable power in combination with hydrogen storage can help provide long-term seasonal flexibility starting from 2030 onwards and would provide an estimated storage capacity of 2000 TWh by 2050).

Flexibility will also be provided through additional measures, including grid expansion and operational measures, demand-side flexibility, power-to-heat, and other sector couplings. Smart solutions, such as smart charging of electric vehicles, can greatly facilitate the integration of VRE by leveraging storage capacity and the flexibility potential of the demand side. Such solutions may include the following.

IRENA has identified 30 flexibility options that may be combined into comprehensive solutions, considering the specifics of national and regional power systems. As more countries adopt ambitious policy targets of very high or 100 percent renewables, adopting such a systemic approach to innovation will become more important.

What kind of technological innovations will support achieving Paris Climate Agreement targets? Is the global energy ecosystem getting there or there's a long way to go?

Most of the technologies needed for an energy system producing net-zero emissions of carbon dioxide are already available. Although their costs must be further reduced, their deployment can be accelerated through innovations – and it is imperative to ramp up deployment now.

Significant progress has been made in electric mobility, battery storage, digital technologies, and artificial intelligence, among others. These shifts are also drawing greater attention to the need for sustainable exploitation and management of rare earth

and other minerals, and investment in the circular economy. New and smart grids, ranging from mini to super grids, bolstered by facilitative policies and markets, are enhancing the power sector's ability to cope with the variability of renewables.

In the light of growing attention for green hydrogen use, priorities for technological innovation include electrolysis integration with ammonia and liquid synthesis, fuel cells for trucks, direct reduction of steel, ammonia-fueled ships, Hydrogen ships, high-temperature electrolysis among others.

Innovation and scale are needed to reduce the costs and diversify the sources of biomass supply and broaden production sustainably. For example, there is a need to further develop conversion technologies to use alternative feedstocks.

Another priority is to develop innovative and alternative ways to reduce material use and reuse and recycle components such as PV panels, wind turbines, batteries, and electrolysers at the end of their lifetime.

Beyond technological development, a systemic approach to innovation – one that pairs technology with innovations in regulatory frameworks, business models, and systems operation is critical to successfully transition to a net-zero carbon world by 2050.

What kind of sector-wise strategies can be adopted towards effective energy transition and decarbonization?

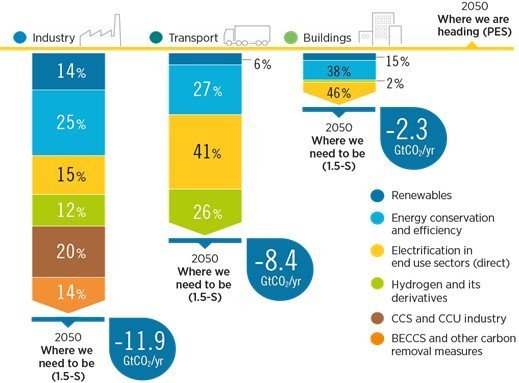

IRENA's analysis shows that a range of technologies and strategies need to be deployed in parallel to reach net-zero carbon emissions by 2050. Renewables will play a dominant role in power and all end-use sectors such as electricity, green hydrogen, or synthetic fuels produced from green hydrogen. Bioenergy and biomass feedstocks will also play an increasing role notably in industry and the transport sector.

In industry, renewable electricity and bioenergy, clean hydrogen, and carbon dioxide (CO2) management solutions such as carbon capture and storage (CCS) and bioenergy with carbon capture and storage (BECCS) play an important role. Energy-intensive industries may relocate to sites with access to low-cost renewable energy. In our 1.5°OC scenario, the total share of renewables in the industry grows to 66 percent of final consumption by 2050 (including non-energy uses).

In the transport sector, direct electrification dominates cars and commercial road vehicles while ammonia from green hydrogen and renewable methanol dominate shipping. In aviation, a mix of synthetic fuels and biofuels will be needed. Whereas total electricity will account for 49 percent of the transport sector's final demand (90 percent of which is renewable) and biofuels for 24 percent, synthetic fuels raise renewables' share to 82 percent of final consumption in transport by 2050.

In the buildings sector, efficiency dominates. This encompasses a major retrofit of buildings as well as efficient space cooling devices and appliances. These must be combined with heat pumps for space and water heating. Traditional biomass cooking stoves are largely replaced with electricity, and to a lesser extent with green gas and modern biomass cooking stoves. The share of electricity in buildings grows to 73 percent and the total share of renewables in buildings grows to 89 percent of final consumption by 2050.

The shift from fossil fuels to electricity and other forms of modern renewable energy is a major efficiency driver, resulting in a significant drop in global energy use for transport and buildings while industrial final consumption increases slightly.

What kind of steps needed to be taken to accomplish the 2030 agenda for Sustainable Development and secure a fighting chance for a 1.5-degree world?

Investment and policy choices in the coming decade will define the pathway to 2050. The window of opportunity to achieve the 2030 emission milestone set out by the IPCC is small, and the choices made in the coming years will determine whether a 1.5°C future remains within reach. This Outlook is guided by the UN's Agenda for Sustainable Development and the Paris Agreement on Climate Change.

Several prerequisites underpin the theory of change behind IRENA's 1.5°C Pathway:

- Pursuing the path that is most likely to drive down energy emissions in the coming decade and put the world on a 1.5°C trajectory.

- Supporting emerging technologies is most likely to become competitive in the short-term and most effective in achieving emissions reductions in the long term.

- Limiting investments in oil and gas to facilitate a swift decline and a managed transition.

- Reserving carbon capture and storage technologies for economies heavily dependent on oil and gas and as a transitional solution where no other options exist

- Phasing out coal and fossil fuel subsidies.

- Adapting market structures for the new energy era.

- Investing in a set of policies to promote resilience, inclusion, and equity and protect workers and communities affected by the energy transition.

- Ensuring all countries and regions have an opportunity to participate in and realize the benefits of the global energy transition.

Spotlight